Canada - FR

Canada - FR U.S. - EN

U.S. - ENEquity markets delivered positive returns in the first quarter of 2024, fueled in part by lower inflation and expectations of rate cuts. As we anticipated, forecasts of an economic downturn have not materialized, and instead, the likelihood of a soft-landing scenario has increased over the past several quarters. Economic prospects for the year ahead vary by country and region but, on balance, the outlook for the world economy is constructive. A comprehensive review of our global economic forecast is detailed in the April edition of our Economic and Capital Markets Outlook. Despite record highs for the S&P 500 and S&P/TSX indices during March, our asset allocation strategy remains unchanged. We are confident that our equity portfolios will continue to outperform cash and bonds over the medium term.

Letko Brosseau Equity Portfolios Offer Value and Growth Opportunities

Our investment strategy revolves around two key principles: focusing on companies that are undervalued and those with the potential for strong growth. As active managers, we regularly adjust our portfolio to adhere to this strategy, reinvesting profits into new opportunities to maintain diversification and attractive valuations. Consequently, our portfolios typically trade at significant discounts to market-weighted global indices which can become expensive and overly concentrated. Indeed, at the end of March, the Magnificent Seven stocks accounted for a remarkable 29.1% of the S&P 500 and traded at a weighted average multiple of 21.8 times forward earnings. This combination of index concentration and lofty valuations warrant a degree of caution in our view.

Notwithstanding our focus on ensuring we avoid overpaying, our investment team actively seeks out growth opportunities trading at reasonable prices. As highlighted in our March 2024 Portfolio Update, sustainable growth is attainable by investing in leading companies trading at discounted multiples, effectively reducing risk exposure.

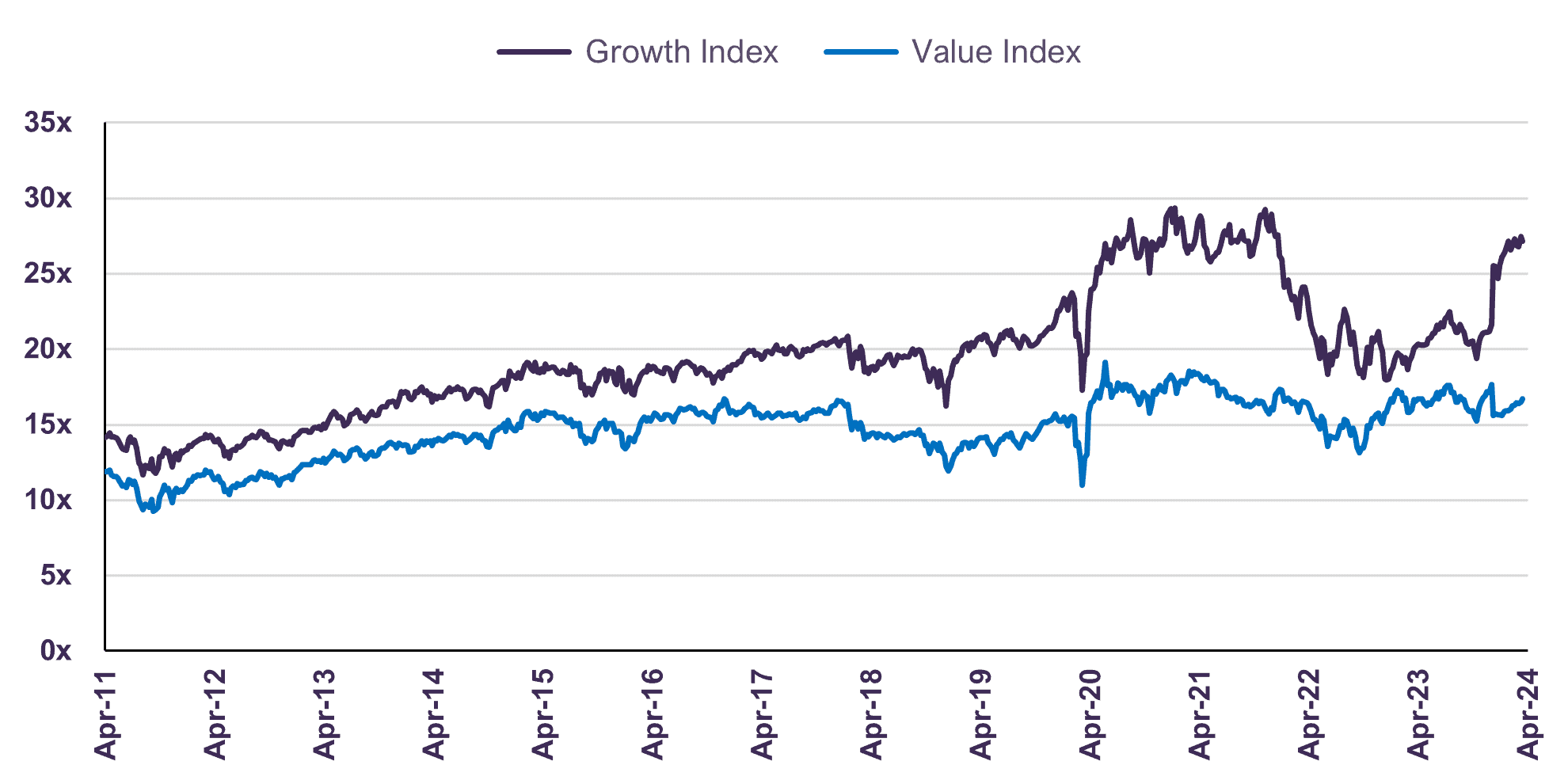

Chart 1 illustrates that the forward price-to-earnings ratio for the S&P 500 Growth Index has surpassed its historical average, whereas the S&P 500 Value Index, more aligned with our equity portfolio’s historical valuation range, remains reasonably priced. In our view, this level of differentiation – valuations are elevated in some substantial parts of the market, but not uniformly expensive – presents a conducive environment for price-sensitive investors with a longer horizon. Thus, despite recent market highs, we continue to see many attractively priced investment opportunities.

S&P 500 Growth and Value Indices

Forward Price-to-Earnings Ratio

Exciting Opportunities in our Equity Portfolios

The companies we hold are a testament to our investment philosophy and exemplify our investment strategy’s core tenets: identifying undervalued companies with meaningful growth potential and strong fundamentals.

The following examples showcase our commitment to balancing value with growth, across all market conditions:

- Linamar is a global manufacturer of highly specialized automotive products, industrial machinery and agricultural equipment. We are confident the company is poised to expand within the automotive sector by increasing its content per vehicle. Furthermore, its substantial backlog of new orders is expected to drive higher sales over the next 2-3 years, an aspect that is currently undervalued by the market. Lastly, within its industrial and agricultural divisions, Linamar’s investments in technology at the product level and in its internal processes are anticipated to lead to both heightened demand in growing markets and higher efficiencies in production. Presently, the company’s stock is trading at a very attractive multiple of 7.7 times forward earnings.

- EDP-Energias de Portugal is a global leader in renewable power and electric distribution utilities, operating in Portugal, Spain, rest of Europe, North America and Brazil. EDP generates over 90% of its EBITDA from stable and highly contracted renewable assets and regulated utilities, allowing it to pay a steady and growing dividend. The company is growing its renewable business by investing in new wind and solar projects, while maintaining capital discipline and a strong balance sheet. EDP-Energias de Portugal currently trades at 12.1 times forward earnings, with a 5.6% dividend yield.

- Manila Water provides clean water and sewage services in the East Zone of Manila in the Philippines. The company serves a total estimated population of over six million people in 23 cities spread over 1,400 square kilometers. Manila Water is one of the most efficient water companies within the emerging markets with a water loss ratio of only 11%, helping them win the trust of provincial governments and new concessions outside of the Manila area. We believe that Manila Water is well positioned to benefit from the long-term demand for these services as there continues to be strong demand for clean water and sewerage services in the Philippines. The company currently trades at 7.1 times forward earnings, with a 4.7% dividend yield.

Concluding Thoughts

Companies trading at elevated valuation multiples rely on aggressive forecasts of future earnings growth over a long horizon. These firms are vulnerable to share price declines if actual growth falls short of expectations. Our risk mitigation strategy entails avoiding these companies and, when evaluating a company’s growth prospects, emphasizing the next 3-5 years as opposed to longer-term projections. Our equity portfolio is valued at 12.6 times forward earnings and offers a 3.3% dividend yield. According to FactSet data, our equity portfolios are also anticipated to deliver earnings growth above their respective indices. We are confident this disciplined investment strategy will contribute to the preservation and growth of your capital.

Invest in Canada

On a separate note, we remain active in our Invest in Canada campaign, aimed at opening a discussion about a worrying trend: the declining level of domestic investment by Canada’s largest pension funds and its impact on the economy. Last month, an open letter, signed by over 90 Canadian business leaders, was sent to the country’s finance minister and her provincial counterparts, urging the need to address this decline. The letter garnered significant attention and spurred an important debate across the country. We welcome this constructive discussion and invite you to watch Letko Brosseau President Daniel Brosseau’s conversation on BNN. Over the past century, Canada’s stock market has been among the best places to invest from a risk-return perspective. Pension funds, the country’s largest pool of long-term capital, should recognize this. We encourage you to learn more about this campaign by reading our Invest in Canada Client Letter.

Where the information contained in this presentation has been obtained or derived from third-party sources, the information is from sources believed to be reliable, but the firm has not independently verified such information. No representation or warranty is provided in relation to the accuracy, correctness, completeness or reliability of such information. Any opinions or estimates contained herein constitute our judgment as of this date and are subject to change without notice.

Past performance is not a guarantee of future returns. All investments pose the risk of loss and there is no guarantee that any of the benefits expressed herein will be achieved or realized.

The information provided herein does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information.

This presentation may contain certain forward-looking statements which reflect our current expectations or forecasts of future events concerning the economy, market changes and trends. Forward-looking statements are inherently subject to, among other things, risks, uncertainties and assumptions regarding currencies, economic growth, current and expected conditions, and other factors that are believed to be appropriate in the circumstances which could cause actual events, results, performance or prospects to differ materially from those expressed in, or implied by, these forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements.

Concerned about your portfolio?

Subscribe to Letko Brosseau’s newsletter and other publications: