Canada - FR

Canada - FR U.S. - EN

U.S. - ENTo invest, or not to invest in oil?

That is the question

March 24, 2021

Investing in oil companies at a time when climate change poses an existential threat and electric vehicles (EVs) are gaining traction raises two important questions. Do such investments still make sense financially? More importantly, are they ethical? We pondered these questions to determine whether we should join in the global movement for fossil fuel divestment or maintain clients’ oil investments.

Read the full report at www.lba.ca/perspective/report-on-oil-investments/.

The answer is yes—for now

The COVID pandemic brought many industries to their knees in 2020, but not that of EVs. While global car sales were down 15% y/y overall, EV sales were up an impressive 50%, ripping market share away from the internal combustion engine (ICE) segment.

The strong sales numbers, continued technological improvements and bold actions by policymakers have raised expectations of EV market penetration. Goldman Sachs predicts 24% of passenger vehicle sales will be electric[1] by 2030 and Bloomberg predicts 28%, while the IEA’s two main scenarios range between 17% and 33%.

Our own analysis indicates that if car companies and governments achieve their current goals, 37% of new passenger car sales will be electric by 2030.

In this context, risks to the oil market are rising. So, if one owns oil equities, one must contemplate the evolution of oil prices under a rapid EV uptake scenario, regardless of its likelihood.

This report considers one such scenario—one in which EV sales rise rapidly to reach 50% of total passenger vehicle sales by the year 2030. It asks how oil demand would be affected, and whether investing in oil still makes sense financially.

In the end, we find it difficult to escape the counterintuitive conclusion that oil demand will likely still be higher in 2030 than the pre-pandemic all-time high of 100 million barrels per day (Mb/d) reached in 2019.

On the arguably more important question of ethics, we find that ignoring the oil market as investors does little to alter the fact of climate change, while engaging with oil companies allows us to remind the industry of its environmental obligations.

How a 50% EV penetration would impact passenger vehicle oil demand

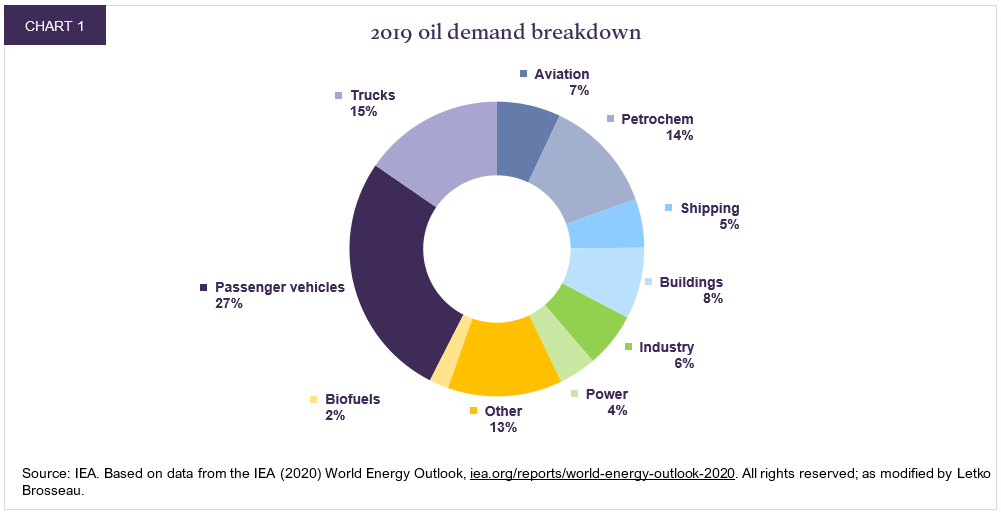

Roughly 1.18 billion internal combustion engine (ICE) passenger vehicles made up 27.1 Mb/d, or 27% of oil demand in 2019 (Chart 1). Under the aggressive EV uptake scenario, we actually believe there would likely still be around the same number of ICE cars on the roads as there are today. But after factoring in assumed annual fuel efficiency gains of 2.0% (the recent annual average is 1.4%), we calculate an oil demand decline of 3.8 Mb/d, or 14%, to 23.3 Mb/d.

What about the rest of the oil market?

But to see how much of a dent this 3.8 Mb/d shortfall puts in oil demand, one must look beyond passenger vehicles, to the remaining roughly three quarters of the oil market that has nothing to do with cars.

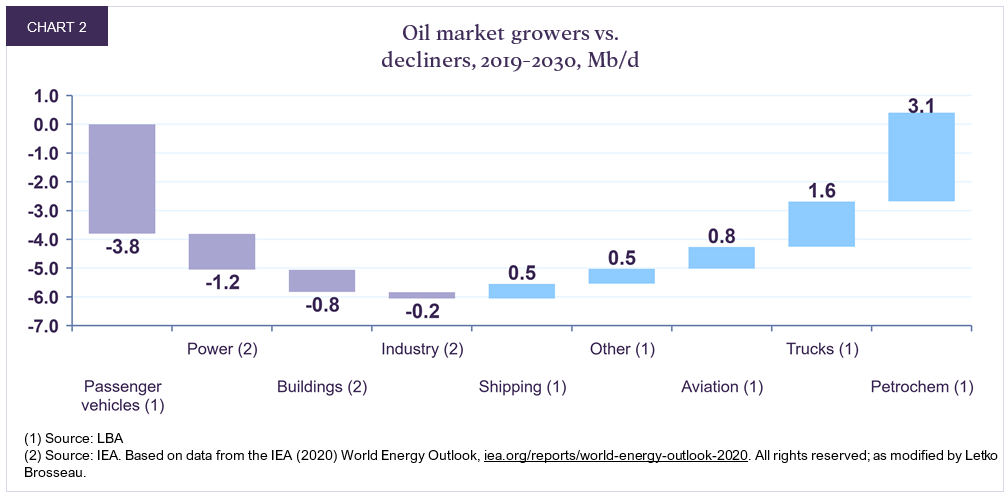

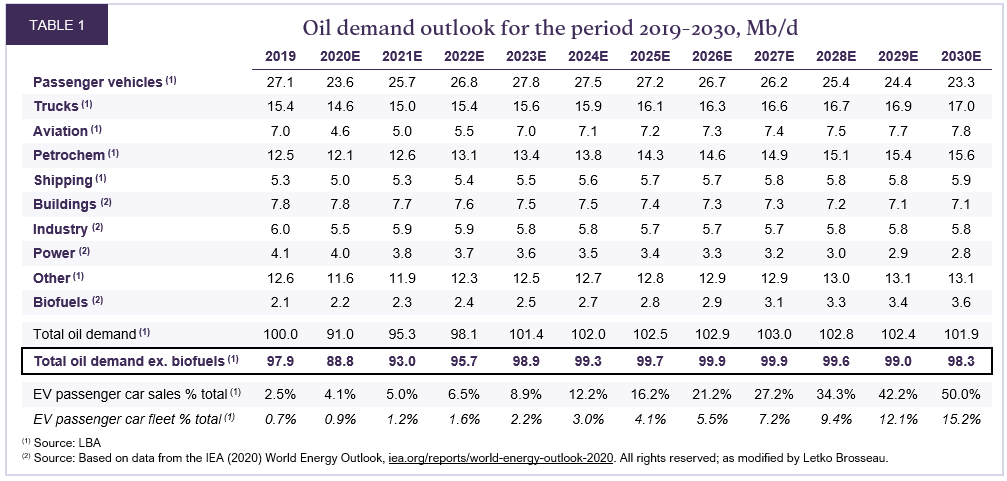

Even under the high EV adoption scenario, we estimate that oil demand gains of 6.5 Mb/d from growing segments (trucking, petrochemicals, air travel, shipping and other) still slightly offsets a 6.1 Mb/d drop from declining segments (passenger vehicles, buildings, industry, and power) (Chart 2). Thus, after taking into account increased biofuels penetration, our analysis pegs crude oil demand at 98.3 Mb/d in 2030 versus 97.9 Mb/d in 2019 (Table 1).

How can the oil market be larger in 10 years than it is today, even under this high EV adoption scenario? One reason is that it takes years for the global vehicle fleet to turn over: we estimate that only 15% of cars on the road will be electric by 2030 in this scenario even though sales reach 50%.

But a more meaningful takeaway follows from sifting through each of the oil market’s sources of demand: oil simply lacks readily scalable substitutes. In order to argue that oil demand will decline this decade, one must put forth that significant portions of the heavy-duty trucking, airplane or maritime fleets will run on alternative technologies that do not yet exist, or are nascent and unlikely to scale fast enough. Or, for instance, that plastic consumption will fail to sharply penetrate emerging markets despite rising living standards. These hypotheses are simply hard to defend, which speaks to oil’s uniqueness as a portable, dense and versatile source of energy.

The oil market’s resilience has implications for climate change…

Unfortunately, our analysis shows that the oil market is unlikely to carry its weight in the fight against climate change, at least over the next decade. According to the Intergovernmental Panel on Climate Change (IPCC), primary energy consumption from oil will have to decrease by 8%[2] by 2030 relative to 2010 levels to achieve emission reduction goals that would limit climate change to a 1.5 degree warming scenario. That’s a crude oil market of around 80 Mb/d, implying a massive 20% decline by 2030.

In this light, our analysis of the oil market’s stickiness is extraordinarily sobering if also disheartening. But confronting this reality at least allows us to ponder what to do about it. On the one hand, it underscores the desperate need to decarbonize the vehicle fleet as fast as possible. On the other, it informs us that the more likely path to limiting global warming to 1.5 degrees is for the renewable power sector to take on an even greater role in displacing emissions from natural gas and especially coal. It also means that carbon capture and sequestration may be even more important than currently envisioned.

… as well as oil prices…

Believing that demand is at least unlikely to decline over the next decade goes a long way towards a constructive price outlook. But we must also consider supply. After years of underinvestment and a pandemic year in which many oil companies slashed capital spending to the bone and others announced a relative shift in capital allocation away from the sector altogether (e.g., BP and Shell), we are doubtful that the supply side will have many low-cost options at its disposal to meet rising demand.

We thus believe the market could tighten significantly once the effects of the pandemic have receded. We believe the marginal cost needed to bring on additional supply to meet demand is at least $60 WTI; we assume WTI oil will average $60 this decade, even though we see substantial upside potential.

… and oil equities

Many oil companies are tremendously profitable at a $60 oil price. On average, we estimate that our portfolio companies would generate a free cash flow yield of 25% and trade at just 2.9x cash flow in 2022 at $60 oil, based on current share prices. And given renewed industry focus on shareholder returns, we think that more of this excess cash than ever before will be used for dividends and share buybacks instead of drilling new wells. Our energy companies currently yield a healthy 2.5% on average.

As ethical issues pushing investors away from the oil market are unlikely to dissipate, we do not expect oil stocks to again trade in-line with historical valuation multiples. However, we think valuations such as those above still leave ample room for upside. By 2024, we expect an average annual appreciation of 25% for our energy holdings.

Most importantly, what about ethics?

Above, we laid out the case for why oil will not soon go away and why this makes for a compelling investment thesis. But the discussion so far is oblivious to the urgency of the climate problem facing us, and whether we as investors have a role to play.

Herein lies the dilemma: on the one hand, climate change is an existential threat that risks our livelihoods and those of future generations, but on the other, oil is so inextricably linked with our daily lives that it makes undoing our dependence extremely challenging anytime soon. We are under no illusion: these two realities are irreconcilable. Continuing to consume oil helps fuel climate change, but stopping our consumption seems impossible.

So, as investors, what are we to do?

One option that continues to gain traction is to divest from fossil fuels altogether. Many decide out of personal preference not to participate in an industry with such a negative externality, and we respect that. But whether one invests in oil or not, a truck in India will need to move freight, a computer keyboard made of plastic will be bought in China, and fertilizer will be used to grow crops somewhere in Brazil. Oil demand doesn’t care whether we invest in public oil equities or not, so divesting does little to alter the reality of climate change, while at the same time it ignores the reality of our everyday lives.

To be fair, there is a logical element to the divestment strategy: it increases the cost of capital for oil companies, driving up their cost of supply and thus the price of oil. Higher prices make oil less competitive with substitutes, which facilitates the energy transition, or so the thinking goes.

And we do believe this probably would help marginally erode oil’s market share. But we also think that 1) the ultimate effect on oil demand may not materially help mitigate climate change, and 2) the unintended consequence is a tax on the world’s lower-income population. Lower income populations such as emerging market workforces spend a disproportionate amount of their earnings on energy expenses such as commuting to work, heating their homes and cooking. This spending is not discretionary but a fixed cost of living. We cannot think of a less equitable way of driving the energy transition than to force higher living expenses upon those who can least afford it. Purposely driving oil prices higher does just that.

For these reasons, we rather focus on engagement. Instead of turning our backs on the oil market, hoping it goes away, we seek to engage with the industry, to understand what management teams are doing to minimize their impact on the climate. Being owners of these companies allows us to maintain a voice at the table and to push them to prioritize the environment. Divesting would remove this ability.

Many of our portfolio energy companies are indeed addressing climate change, for example through investments in renewables, or emission reduction targets. Would these green initiatives have materialized absent a shareholder base that actively engages them? It’s difficult to know for sure, but it doesn’t hurt at the very least. The planet needs many more such initiatives, and we will push for them on behalf of our clients—but we can only do so if we have a seat at the table.

Conclusion

About a year ago, the world’s largest money manager, Blackrock, made big news by announcing an environmental, social and governance (ESG) overhaul of its investment process. The asset manager put special emphasis on climate change, promising to begin divesting certain fossil fuel companies, such as those producing thermal coal, and to scrutinize the environmental characteristics of its investments like never before. It intends to double its ESG exchange-traded funds over the next few years. In his letter to chief executive officers, CEO Larry Fink argued that due to awareness of climate risks, “we are on the edge of a fundamental reshaping of finance.” We agree.

But beneath the headlines was an important yet overlooked acknowledgement: “the energy transition will still take decades” and “the technology does not yet exist to cost-effectively replace many of today’s essential uses of hydrocarbons. We need to be mindful of the economic, scientific, social and political realities of the energy transition. Governments and the private sector must work together to pursue a transition that is both fair and just—we cannot leave behind parts of society, or entire countries in developing markets, as we pursue the path to a low-carbon world.” (emphasis added)

In writing these words, he was staring down the same two irreconcilable realities that we are.

In our opinion, choosing not to invest in oil companies focuses solely on the reality of climate change while ignoring that of our everyday lives. We, on the other hand, believe the best we can do for our clients and for the planet is to honestly recognize both sides of the coin. In doing so, we can actually help influence the outcome.

We do, however, know that one day—probably sooner than most in the industry would care to admit—the rise of EVs will likely make oil companies uninvestable. So it is not a question of “if,” but “when” one winds down these investments. Here, we only submit that given (1) the resilience of oil demand this decade despite EV sales growth, (2) a sluggish post-pandemic rebound in oil supply, and (3) compelling company valuations, that day has perhaps not yet arrived.

Mentions légales

[1] Refers to both battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs)

[2] We have extrapolated the median decline of the four illustrative model pathways from an IPCC report (see Masson-Delmotte, et. al., 2018, “Global Warming of 1.5 °C. An IPCC Special Report,” in Summary for Policymakers, IPCC. Available at https://www.ipcc.ch/2018/10/08/summary-for-policymakers-of-ipcc-special-report-on-global-warming-of-1-5c-approved-by-governments/.)

All dollar references in the text are US dollars unless otherwise indicated.

The information and opinions expressed herein are provided for informational purposes only, are subject to change and are not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. Any companies mentioned herein are for illustrative purposes only and are not considered to be a recommendation to buy or sell. It should not be assumed that an investment in these companies was or would be profitable. Unless otherwise indicated, information included herein is presented as of the dates indicated. While the information presented herein is believed to be accurate at the time it is prepared, Letko, Brosseau & Associates Inc. cannot give any assurance that it is accurate, complete and current at all times.

Where the information contained in this presentation has been obtained or derived from third-party sources, the information is from sources believed to be reliable, but the firm has not independently verified such information. No representation or warranty is provided in relation to the accuracy, correctness, completeness or reliability of such information. Any opinions or estimates contained herein constitute our judgment as of this date and are subject to change without notice.

Past performance is not a guarantee of future returns. All investments pose the risk of loss and there is no guarantee that any of the benefits expressed herein will be achieved or realized.

The information provided herein does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information.

This presentation may contain certain forward-looking statements which reflect our current expectations or forecasts of future events concerning the economy, market changes and trends. Forward-looking statements are inherently subject to, among other things, risks, uncertainties and assumptions regarding currencies, economic growth, current and expected conditions, and other factors that are believed to be appropriate in the circumstances which could cause actual events, results, performance or prospects to differ materially from those expressed in, or implied by, these forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements.

Concerned about your portfolio?

Subscribe to Letko Brosseau’s newsletter and other publications: