Canada - FR

Canada - FR U.S. - EN

U.S. - ENAs we reach the midpoint of 2024, equity markets have trended upwards as inflation has eased and the global economy continues to show remarkable resilience. Year-to-date, the total return of the S&P 500 is up 19.6% (in Canadian dollars), while the S&P/TSX rose 6.1%, the MSCI EAFE 9.3%, and the MSCI Emerging Markets 11.5%.

Stock market multiples expand as inflation heads lower

With the notable exception of the U.S. Federal Reserve, since the beginning of the year, more than 30 central banks have cut rates and transitioned towards looser monetary policy amid improving inflationary conditions. As noted in our July Economic and Capital Markets Outlook, lower levels of inflation tend to boost equity valuations, and this has been a contributing factor to the markets’ strong year-to-date performance.

In some sectors of the stock market, however, valuation levels have risen to euphoric extremes. The enthusiasm surrounding artificial intelligence (AI) and its transformative potential across various industries has concentrated investor attention on the so-called “Magnificent Seven” tech giants (Apple, Microsoft, Alphabet, Amazon Nvidia, Meta, and Tesla). Indeed, Nvidia’s market capitalization has surged to such an extent that it is now larger than the economies of several countries including Canada, Brazil, and Italy.

Moreover, the Mag-7 have contributed more than 60% of the S&P 500’s year-to-date gains, account for 31% of the index, and trade at an elevated weighted average P/E multiple of 38.8 times. A similar trend has unfolded within Emerging Markets. Notably, Taiwan Semiconductor Manufacturing Company (TSMC), the world’s largest contract chip manufacturer for leading tech firms, including Nvidia, Apple, and Intel, drove nearly half of the MSCI Emerging Markets index’s year-to-date gains. Meanwhile, Tencent, a major Chinese conglomerate involved in e-commerce, cloud computing, entertainment, and internet services, accounted for 15% of the EM benchmark’s year-to-date price return despite geopolitical tensions and regulatory challenges in China’s IT sector. These trends, present in both developed and emerging markets, underscore the significant influence that a small group of technology companies continues to have on market performance, highlighting the need for investors to prudently consider the concentration risk within their portfolios and ensure effective diversification.

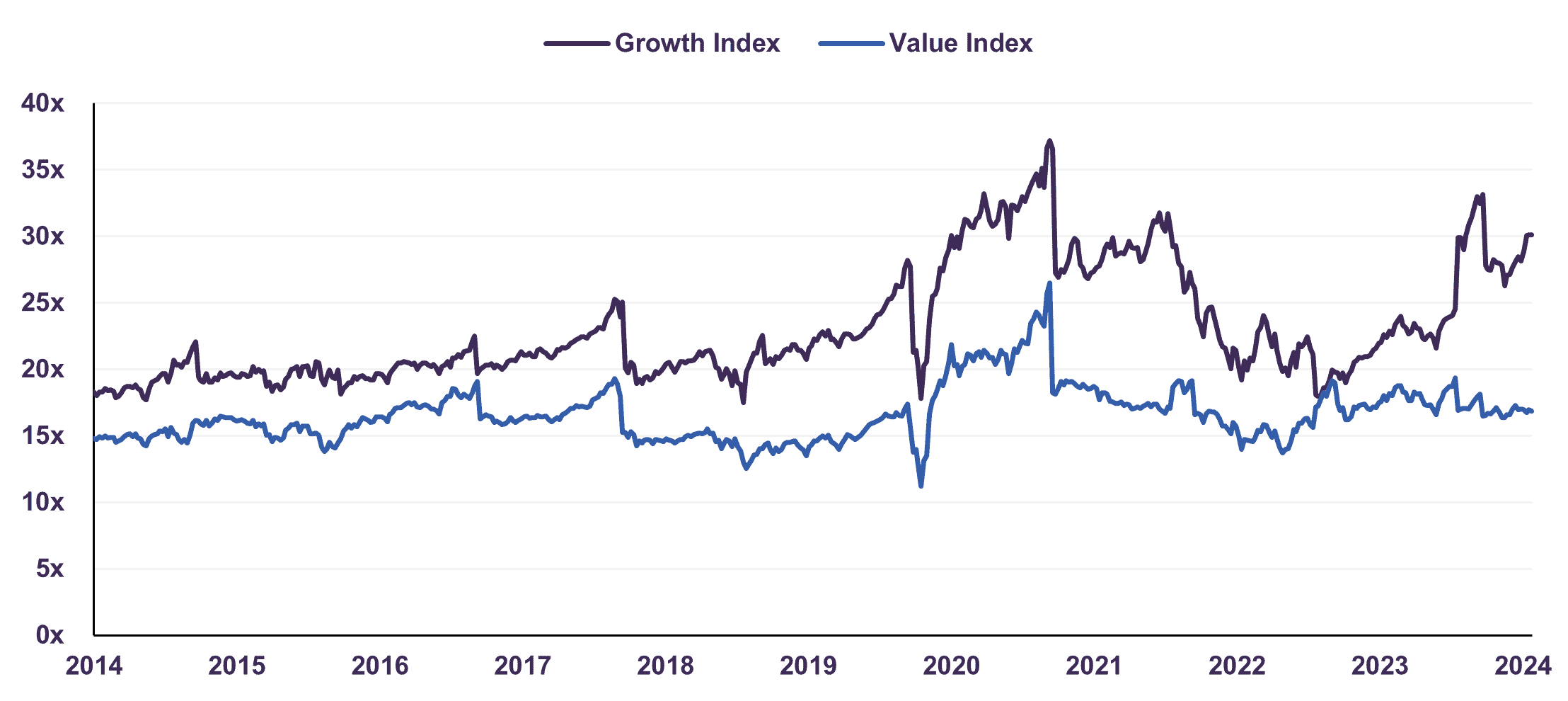

Finding Value in Growth

The S&P 500 Growth Index has surpassed its last ten-year average of 23.0 times forward price-to-earnings, whereas the S&P 500 Value Index remains attractively priced and within range of its ten-year average of 16.6x (Chart 1). As of the end of June, the S&P Growth Index trades at 30.1 times forward P/E, nearly double the S&P Value Index, which currently sits at 16.9x. We do not believe that stocks are expensive across the board and there remain opportunities for price-sensitive investors with a longer horizon, despite recent market highs.

S&P 500 Growth and Value Indices

Forward Price-to-Earnings Ratio

Concluding Thoughts

As active discretionary managers, we focus on constructing well-diversified portfolios of attractive companies, while avoiding undue concentration exposure to a certain group of companies or sectors. This strategy has been shown to protect against asset bubbles and overvaluation. Our investment team has been able to generate strong absolute returns within our equity portfolios, while prudently mitigating undue risk. The Letko Brosseau Global Equity portfolio has delivered a 14.1% return over the last twelve months as of the end of June and trades at just 12.6 times forward earnings, while offering a 3.4% dividend yield. Our asset allocation strategy remains unchanged. We are confident that our equity portfolios will continue to outperform cash and bonds over the medium term.

Where the information contained in this presentation has been obtained or derived from third-party sources, the information is from sources believed to be reliable, but the firm has not independently verified such information. No representation or warranty is provided in relation to the accuracy, correctness, completeness or reliability of such information. Any opinions or estimates contained herein constitute our judgment as of this date and are subject to change without notice.

Past performance is not a guarantee of future returns. All investments pose the risk of loss and there is no guarantee that any of the benefits expressed herein will be achieved or realized.

The information provided herein does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information.

Certain information contained in this document constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “target,” “project,” “estimate,” “intend,” “continue” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of the strategy(ies) may differ materially from those reflected or contemplated in such forward-looking statements.

The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com).

The S&P/TSX Index is a product of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”) and TSX Inc., and has been licensed for use by Letko, Brosseau & Associates Inc. Standard & Poor’s® and S&P® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by Letko, Brosseau & Associates Inc. TSX® is a registered trademark of TSX Inc., and have been licensed for use by SPDJI and Letko, Brosseau & Associates Inc. Letko, Brosseau & Associates Inc.’s product is not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates, or Bloomberg and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the S&P/TSX Index.

Concerned about your portfolio?

Subscribe to Letko Brosseau’s newsletter and other publications: