Canada - FR

Canada - FR U.S. - EN

U.S. - EN

Portfolio Update

August 10, 2022

Global equity markets delivered positive returns during the month of July, following a difficult first half of the year. Geopolitical risk, high inflation and monetary policy tightening have raised fears of a recession taking place in the latter half of this year and 2023. With inflation well above the 2% target, central banks in the developed world remained steadfast in their campaign to raise policy rates. During the month of July, the Federal Reserve and the Bank of Canada increased their benchmark rates by 0.75% and 1%, respectively. As well, the European Central Bank embarked on a path of monetary tightening for the first time in 11 years by raising its key interest rate to 0% from -0.5%. Investors seem to have perceived these inflation-lowering measures as reassuring: the S&P 500 climbed 8.5% (in Canadian dollars), the S&P/TSX rose 4.7% and the MSCI World gained 5.6% during the month of July. These gains suggest the possibility of a recession scenario was largely priced into the market during the first half of the year. As highlighted in our most recent Economic and Capital Markets Outlook, the likelihood and severity of a possible recession differ across economies, with the United States and Canada relatively well positioned to address current headwinds.

Our portfolios continue to outperform their respective benchmarks on a year-to-date basis. We owe this to an investment strategy that favours market-leading companies that have the balance sheet strength to weather challenges in the broader economy and that trade at attractive valuations. We invest in these companies over securities that are either overly sensitive to rising interest rates or trade well above their intrinsic value.

Risks of a Short-Term Focus

“The stock market is a device for transferring money from the impatient to the patient.”

Warren Buffett

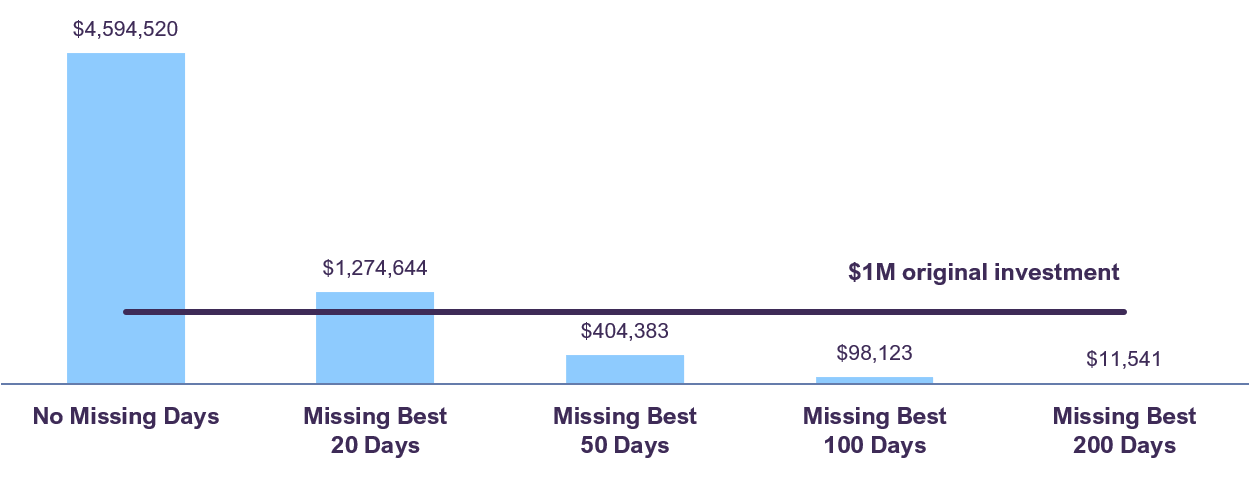

Much has been written in the realm of behavioral finance about an investor’s tendency to revert toward short-termism. One way this can manifest itself is the insistence on trying to time the market rather than focusing on long-term growth by remaining invested in the market. In periods of volatility, such as the one we are currently experiencing, this may seem like a tempting investment tactic. However, the process of selling your risky investments and temporarily shifting to cash ultimately entails two very difficult decisions: when to sell and when to re-enter the market. These decisions are almost impossible to time perfectly as no one knows with certainty when the market has reached its highest and lowest points. Chart 1 shows the impact on a hypothetical $1 million investment when the best 20, 50, 100 and 200 days in the market were missed over the 20-year period ending July 31st, 2022. An investor who remained fully invested in the market over the period generated an annualized return of 7.9% while an investor who missed the 20 best days returned just 1.2% annually.

Furthermore, an investor who missed the 50, 100 and 200 best days generated negative returns. Investors who shift their portfolio to cash and try to time when to re-enter the market incur the risk of missing the market’s biggest gains. Remaining invested through both the bull and bear markets is crucial to long-term success – timing these cycles is not.

Staying Invested

Value of a hypothetical $1M investment in the

S&P 500 from August 2002 to July 2022

Based on equity prices as of July 31st, 2022. Sources: Factset (www.factset.com) financial data and analytics and LBA calculations.

Portfolios with Lower Valuations Tend to Provide Better Protection in an Economic Slowdown

Our analysis has shown that companies trading at lower multiples of earnings perform relatively better than those trading at higher multiples during periods of slowing GDP growth. Although the level of outperformance varies over time, low-valuation stocks have typically provided better downside protection in most economic slowdowns since World War II. In general, our companies have lower valuations and higher yields than the underlying market

(Table 1).

Projected key metrics of companies in Letko Brosseau equity portfolios and their benchmark indices

Based on equity prices as of July 31st, 2022. Sources: Factset (www.factset.com) financial data and analytics and LBA calculations, Letko Brosseau Canadian Equity Fund, Letko Brosseau International Equity Fund.

Past economic slowdowns have been attributed to a variety of factors, among them are elevated inflation and interest rate increases. Our portfolios are made up of market leaders that are well positioned to weather the impacts of both over the long term. Companies we view as overvalued are often priced to reflect unsustainable growth targets. As companies contend with the current inflationary environment, growth targets become more difficult to achieve, and overvalued companies face greater downward price pressure. Additionally, increases in interest rates lead to higher borrowing costs. We believe the companies in our portfolios have the balance sheet strength to absorb these higher interest costs and allocate excess capital effectively.

Concluding Thoughts

Patience in the face of volatility will continue to benefit investors over the long term – the longer the time frame, the greater the likelihood of a positive outcome. We seek to construct our portfolios with this approach in mind, where short-term market gyrations are viewed as opportunities to increase our position in companies with solid fundamentals that we believe will perform well over time.

Legal notes

The information and opinions expressed herein are provided for informational purposes only, are subject to change and are not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. Any companies mentioned herein are for illustrative purposes only and are not considered to be a recommendation to buy or sell. It should not be assumed that an investment in these companies was or would be profitable. Unless otherwise indicated, information included herein is presented as of the dates indicated. While the information presented herein is believed to be accurate at the time it is prepared, Letko, Brosseau & Associates Inc. cannot give any assurance that it is accurate, complete and current at all times.

Where the information contained in this presentation has been obtained or derived from third-party sources, the information is from sources believed to be reliable, but the firm has not independently verified such information. No representation or warranty is provided in relation to the accuracy, correctness, completeness or reliability of such information. Any opinions or estimates contained herein constitute our judgment as of this date and are subject to change without notice.

Past performance is not a guarantee of future returns. All investments pose the risk of loss and there is no guarantee that any of the benefits expressed herein will be achieved or realized.

The information provided herein does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information.

This presentation may contain certain forward-looking statements which reflect our current expectations or forecasts of future events concerning the economy, market changes and trends. Forward-looking statements are inherently subject to, among other things, risks, uncertainties and assumptions regarding currencies, economic growth, current and expected conditions, and other factors that are believed to be appropriate in the circumstances which could cause actual events, results, performance or prospects to differ materially from those expressed in, or implied by, these forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements.

Concerned about your portfolio?

Subscribe to Letko Brosseau’s newsletter and other publications: