Canada - FR

Canada - FR U.S. - EN

U.S. - EN

Portfolio Update

April 8, 2022

Global equity markets partially recovered from the initial selloff following Russia’s invasion of Ukraine in February. Year to date, the S&P 500 Index is down 5.7% in Canadian dollar terms, the S&P TSX is up 3.8% and the MSCI World Index is down 6.2%. Longer-duration fixed income securities have continued to show weakness as monetary policy has begun to normalize. Notably, the 30-year Government of Canada bond suffered a 15% loss over the last three months as its yield rose 70 basis points. Our investment strategies have performed well, in large part due to our exposure to commodity and defensive sectors, shorter maturity fixed income securities, and the avoidance of companies trading at rich valuations.

We continue to believe the global economy will grow despite risks arising from inflation and the conflict in Ukraine. The spillover effect of the Russia/Ukraine war is not expected to be felt equally around the world. Russia and Ukraine will face severe contraction, however, these two countries account for a very small portion of world growth. Meanwhile, Europe is more at risk of an economic slowdown due to its dependence on Russian energy supplies. The economies of the U.S., Canada and China should be sufficiently resilient to withstand higher inflation while avoiding a recession.

Risk to Outlook: Inflation

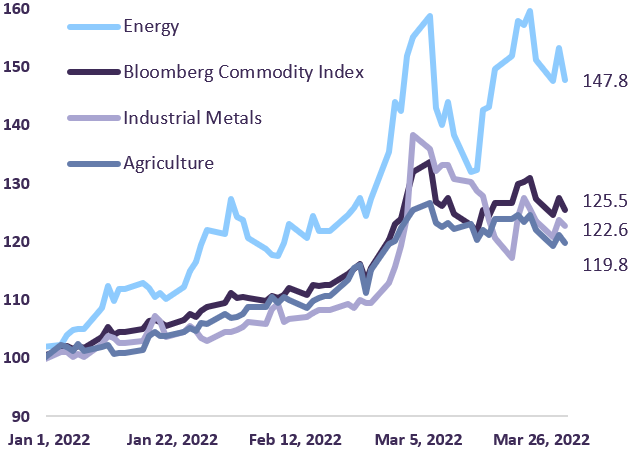

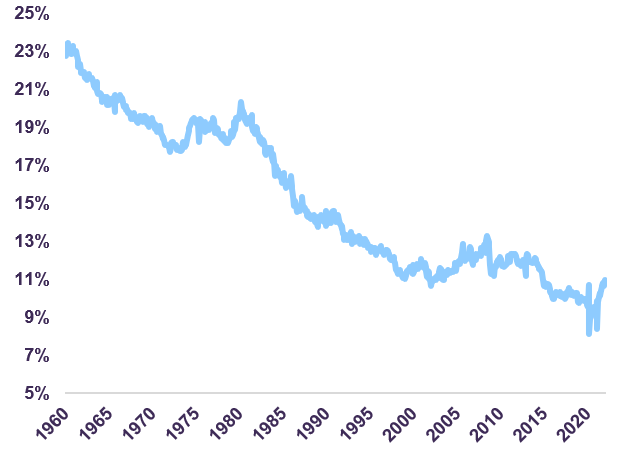

Energy costs and food prices made the largest contributions to headline inflation in the U.S. during the month of February. The U.S. Consumer Price Index (CPI) for all items accelerated to 7.9% year-on-year in February, and we estimate that the short-term impact of higher energy and food prices could add around 2% to CPI, implying headline inflation near 10%. As noted in our “Economic and Capital Markets Outlook – April 2022”, Russia and Ukraine are important producers of agriculture, energy and industrial metal commodities. The price of these commodities has surged on expectations of supply disruptions (Chart 1). As spending on food and energy tends to be inflexible, households will likely have to scale back spending on discretionary items if disruptions, resulting from the war, are sustained. While this raises the risk that growth will be lower than previously expected, it does not imply that a recession is imminent. We note that the share of personal disposable income allocated to food and energy in the U.S. remains well below the historical average (Chart 2). In addition, while savings rates have moderated back to average levels in the U.S. and Canada, excess savings still represent more than 10% of GDP in both countries, suggesting households may have a buffer against elevated food and energy prices.

Commodity Price Indexes

(Year-to-date)

U.S. Food and Energy Expenditure

Share of Disposable Personal Income (nominal)

Risk to Outlook: Geopolitical

Russia and Ukraine account for 1.7% and 0.2% of global GDP in nominal terms, respectively. While these economies will undoubtedly contract sharply due to the conflict and the economic sanctions implemented on Russia, the risk to global growth lies in the spillover effects of the crisis. Europe is vulnerable due to its dependence on Russian energy. Approximately 75% of the EU’s total energy consumption is derived from oil (38%), natural gas (25%) and coal (11%) with Russia supplying 27%, 40%, and 46% of the EU’s imports of these energy sources, respectively.1 A threat to the physical flow of energy products to Europe means supply shortfalls represent a greater risk to economic activity in the region than energy price inflation. The economic risk to the rest of the developed world and emerging market countries is mainly due to inflationary pressures exacerbated by the conflict. We believe the U.S. and Canada are well positioned to navigate the current situation and large emerging markets, such as China and India, should also be able to tolerate these headwinds.

Concluding Thoughts

While the U.S. Federal Reserve and the Bank of Canada’s decision to raise their benchmark interest rates by 25 basis points to 0.5% marks the beginning of a rate tightening cycle, monetary policy remains very accommodative. We believe our portfolios are structured to tolerate higher inflation and some geopolitical risk. Capital preservation and low duration remain the focus of our fixed income strategy as long-term bonds are not an appealing investment in the current environment. In fact, we note that over the last decade, the annualized return on the 30-year Government of Canada bond was only 2.5%. Given that inflation during the period averaged 2.2%, the inflation-adjusted (or real) return was 0.3% per annum, a meager performance even in the context of subdued price pressures. In contrast, the MSCI World Index delivered an average annualized return of 13.5% (in Canadian dollars) over the past 10 years despite the disruptions due to Europe’s debt crisis, a China/US trade war and the global pandemic. We believe our equity portfolios currently trade at very reasonable valuations (11 times 2022 earnings), pay an attractive dividend yield (3%) and should offer meaningful value creation in the medium-term.

1 European Commission Press Release “Questions and Answers on REPowerEU”

Legal notes

The information and opinions expressed herein are provided for informational purposes only, are subject to change and are not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. Unless otherwise indicated, information included herein is presented as of the dates indicated. While the information presented herein is believed to be accurate at the time it is prepared, Letko, Brosseau & Associates Inc. cannot give any assurance that it is accurate, complete and current at all times.

Where the information contained in this presentation has been obtained or derived from third-party sources, the information is from sources believed to be reliable, but the firm has not independently verified such information. No representation or warranty is provided in relation to the accuracy, correctness, completeness or reliability of such information. Any opinions or estimates contained herein constitute our judgment as of this date and are subject to change without notice.

Past performance is not a guarantee of future returns. All investments pose the risk of loss and there is no guarantee that any of the benefits expressed herein will be achieved or realized.

The information provided herein does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information.

This presentation may contain certain forward-looking statements which reflect our current expectations or forecasts of future events concerning the economy, market changes and trends. Forward-looking statements are inherently subject to, among other things, risks, uncertainties and assumptions regarding currencies, economic growth, current and expected conditions, and other factors that are believed to be appropriate in the circumstances which could cause actual events, results, performance or prospects to differ materially from those expressed in, or implied by, these forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements.

Concerned about your portfolio?

Subscribe to Letko Brosseau’s newsletter and other publications: