Canada - FR

Canada - FR U.S. - EN

U.S. - ENMy mother was always careful about what she paid for everything she bought. She was so happy when she found what she wanted on sale and she certainly did not want to overpay. My mother never bought something she thought was poor quality, would not last or was not healthy. She was quite discerning.

In the language of finance, we call this value investing.

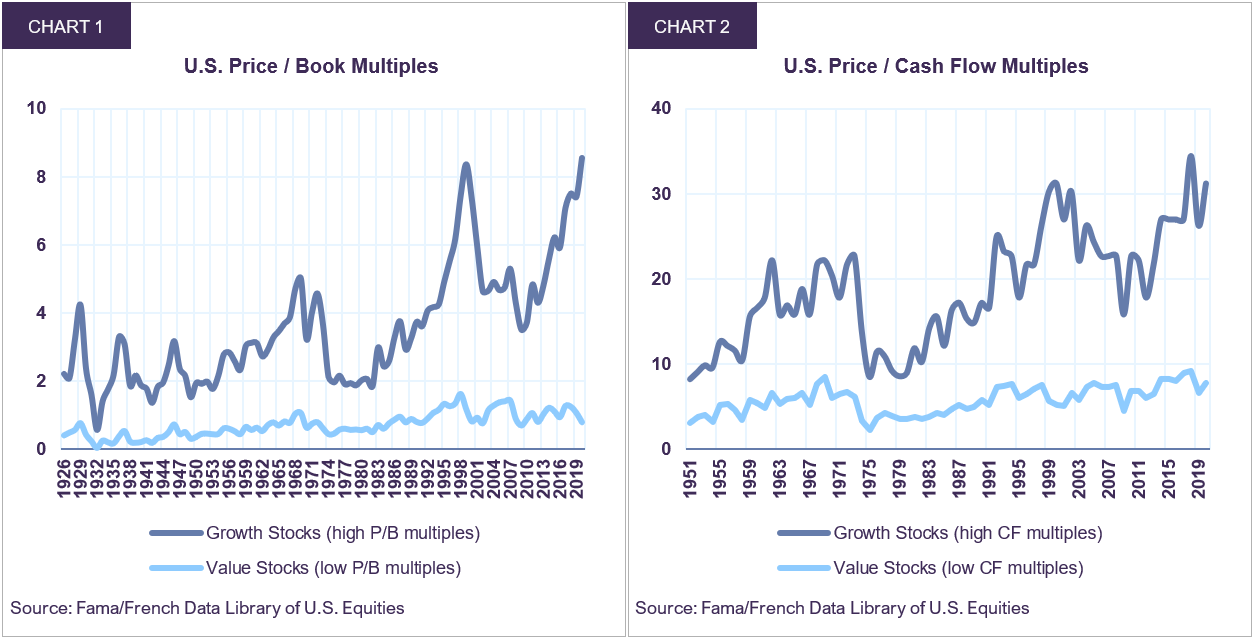

Value stocks trade at low multiples of earnings, cash flows, book value, market-value-to-sales, and offer high dividend yields. Growth stocks, on the other hand, tend to trade at high multiples of earnings, cash flows, book, sales, and provide low dividend yields (Charts 1 and 2)1. A common view is that growth, or more expensive stocks, deserve higher multiples because they promise greater profits in the future, whereas value stocks have already realized on their promise. Two birds in the bush versus a bird in hand.

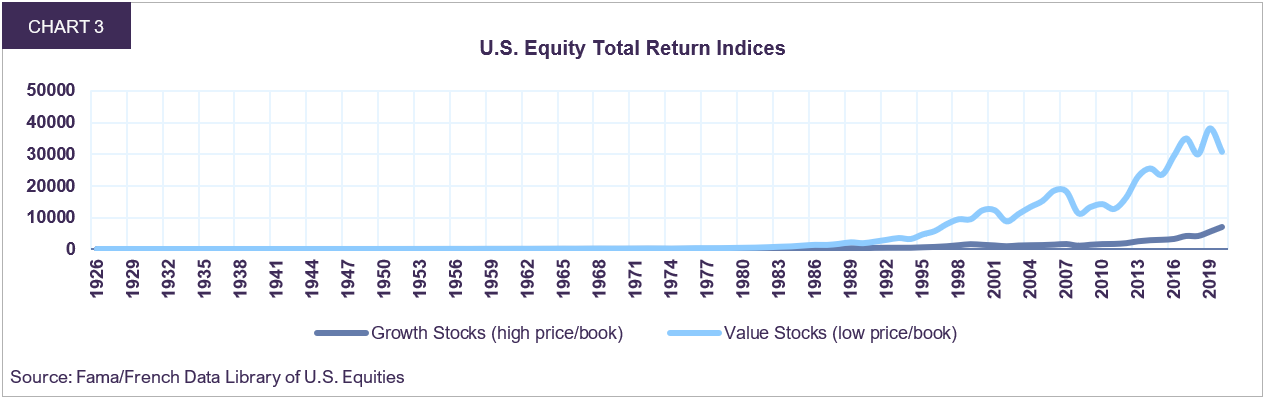

Despite the current appeal of high multiple stocks, the empirical evidence is clear: stocks trading at lower valuations have regularly outpaced expensive equities over the last 90 years, and by a good margin. A dollar invested in higher multiple stocks in 1927 was worth $7,159 by August 2020. The same dollar invested in value stocks was worth $30,774, or 4.3 times more (Chart 3).

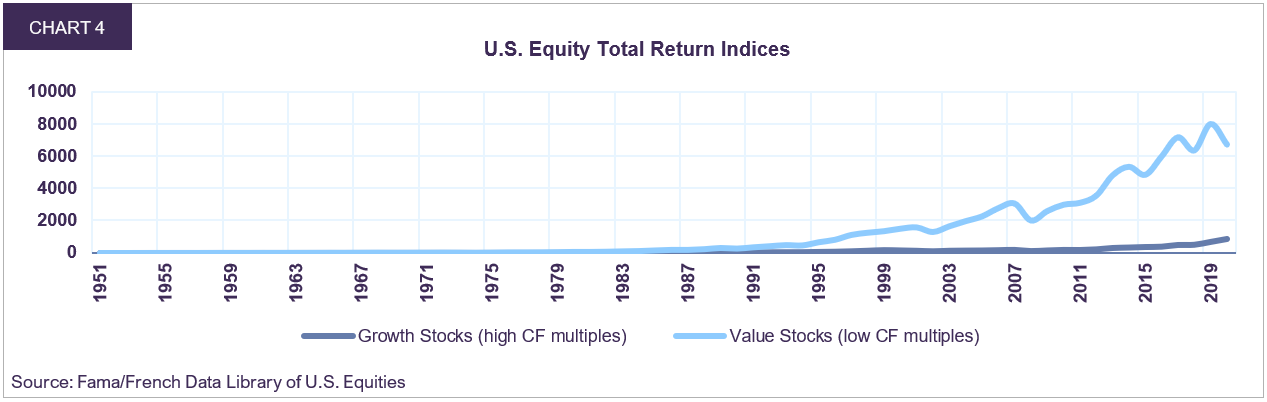

Using cash flow multiples as the metric, growth and value stocks show similar results as above. A dollar invested in growth stocks in January 1952 (earliest data available) was worth $871 by August 2020. The same dollar invested in value stocks was worth $6,735, or almost 8 times more (Chart 4).

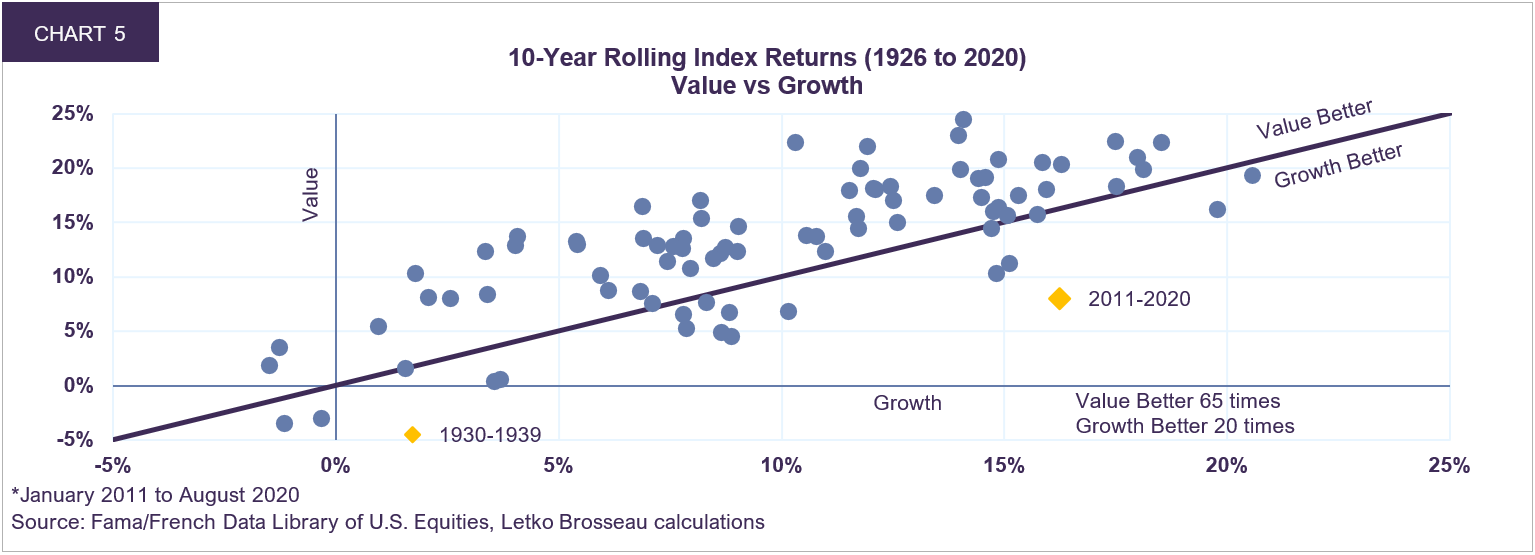

The outperformance of value stocks is remarkably consistent across time. Chart 5 shows the 10-year rolling returns calculated annually since 1936. Each point in the scatter chart represents one 10-year period with the growth return on the horizontal axis and the value return on the vertical axis. The line at 45 degrees crossing through the chart represents all instances where value and growth returns are equal and a point above (below) the line indicates that returns from value stocks were greater (less) than growth. As can be seen in the chart, value stocks beat growth most of the time. In fact, value beat growth more than 3 times as often.

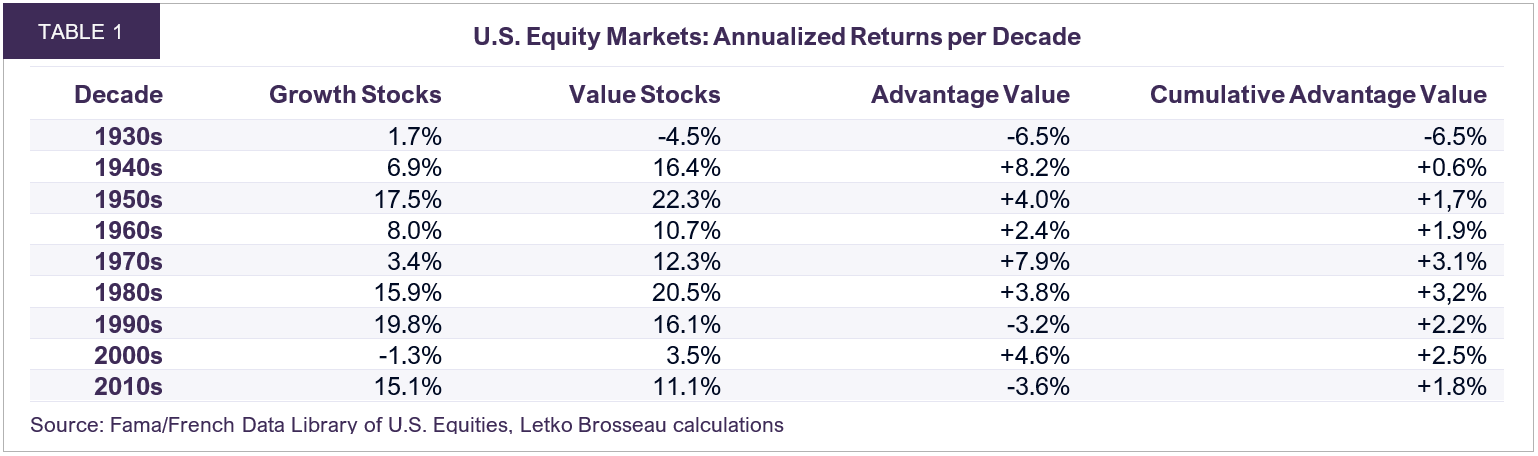

In every decade since the 1930s, value stocks have outperformed growth stocks, except for the depression of 1930s, the tech bubble of the 1990s and the interest rate bubble of the 2010s (Table 1).

So, it looks like my mother was on to something. She understood that it was easy to overpay and many people are ready to offer you what you want at a high price. The challenge was to find real value.

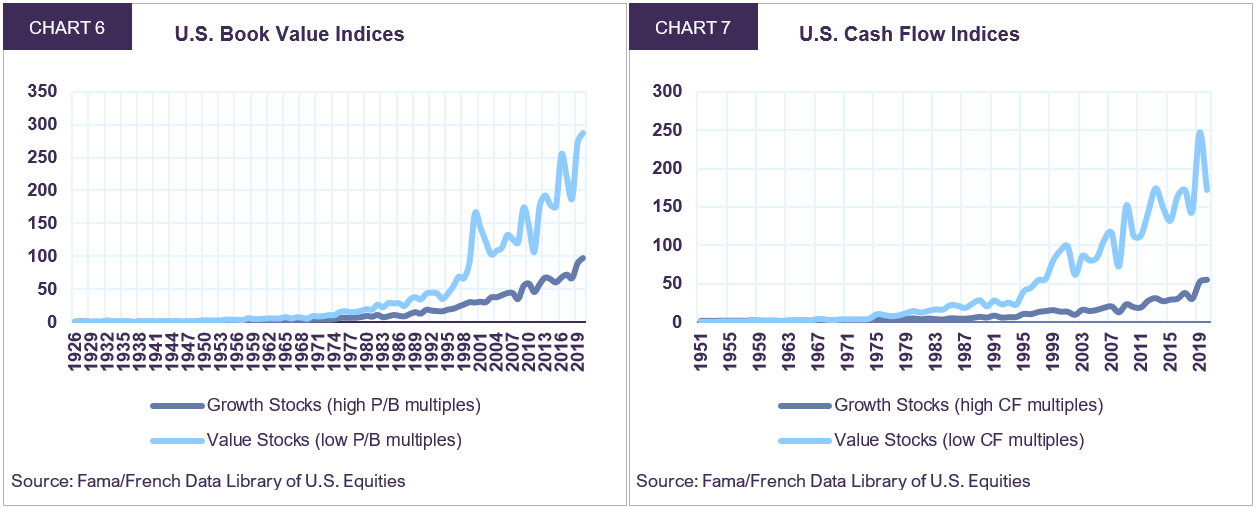

Which brings us to the next question: why have value stocks done better? The answer is not complicated. The only way a stock can really do better over long periods of time is if the underlying business progresses well. We can track a company’s long-term financial success through its book value and cash flows. Using aggregate data, Chart 6 shows that $1 of growth stock book value in 1926 appreciated to $98 by 2020, whereas $1 of value stock book value grew to $287 over the same period, close to 3 times more. Similarly, $1 of growth stock cash flow in 1951 grew to $55 by 2020 while $1 of value stock cash flow rose to $172, 3.1 times more (Chart 7).

So, it appears that value stocks have outperformed over the long-term because their underlying businesses have grown more. What could account for this counterintuitive result? Aren’t growth stocks supposed to grow more?

The first reason value stocks have grown more rapidly is that they generate more earnings and cash, so they invest more. These investments in turn generate more future earnings, cash flows and book value. The second reason is that many growth stocks fail or flounder. Take the cell phone industry for example. Apple is a success story but former market leaders like Blackberry, Nokia, Palm and Motorola stumbled and never sustained their promise2. Google is still thriving but former tech darlings AOL, Yahoo, Netscape, MySpace, AltaVista, Ask and Napster are not. You cannot judge growth stock returns by only those that succeed.

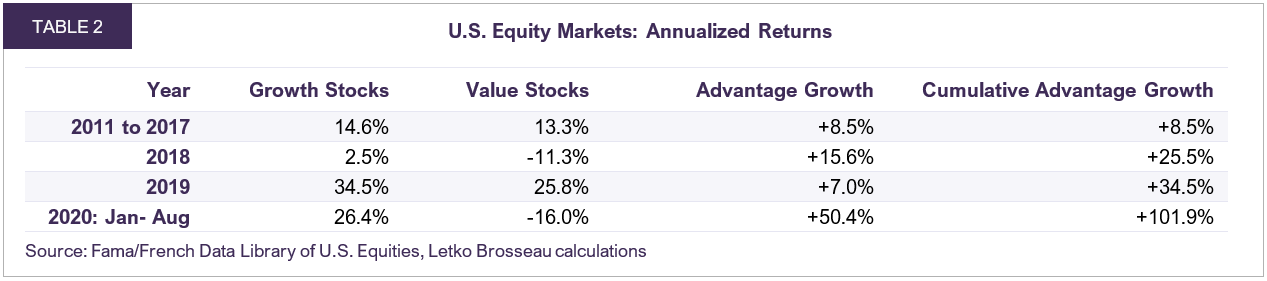

When we look at the relative returns of value versus growth stocks over the last 10 years however, we might be tempted to question our premises. Since the end of 2010, $1 invested in value stocks was worth $2.25 by August 2020, whereas $1 invested in growth stocks was worth $4.54, twice as much. This represents quite a setback for value stocks from the historical norm.

Has the world changed?

In fact, the lag in value returns was very minor in the first seven years of the last decade. Practically all the difference has occurred since 2018 and particularly in 2020 (Table 2). However significant the gap, three years does not beat 90 years.

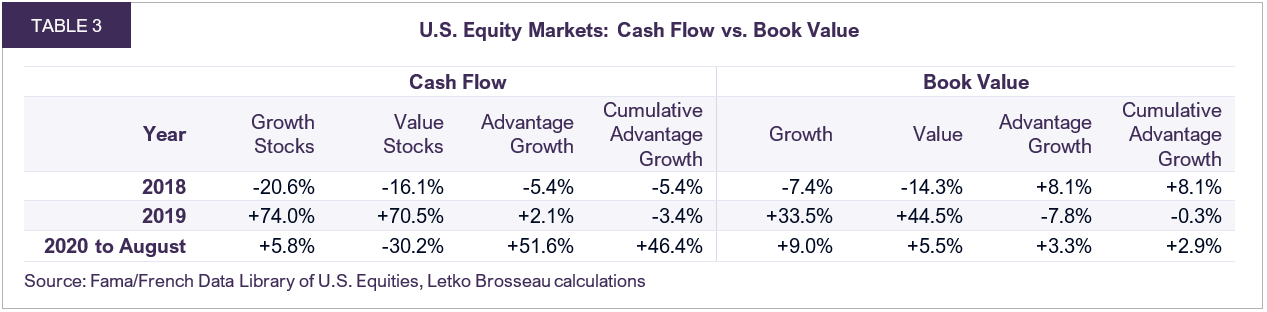

What happened in these last 3 years? Since 2018, the global economy has faced two major headwinds. First, the trade war between the US and China, which engulfed Europe and most of the rest of the World, led to speculation that a recession would result. Then COVID-19 hit which caused an actual recession. We can see in Table 3 that cash flows and book values grew at approximately the same rate over 2018-2019, but cash flows fell precipitously in 2020 with the onslaught of the pandemic recession.

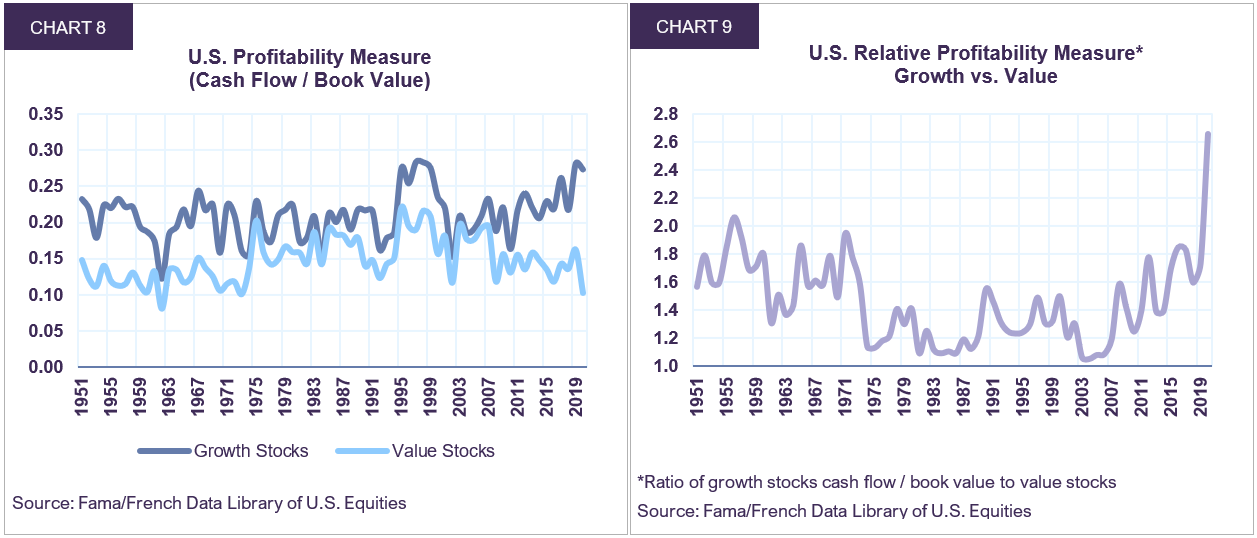

Charts 8 and 9 illustrate that the profitability of growth companies is normally higher than that of value stocks. However, the relative profitability is currently at an abnormal level. The profitability of growth stocks is at the higher end of its historical range, whereas the profitability of value stocks is at the lower end. This is a consequence of the nature of the pandemic recession, which depressed demand for physical goods but increased the demand for services.

The drop in profitability explains only about half (46%) of the relative outperformance of growth stocks to value stocks (86%) over the last three years. But even that is questionable because it assumes that investors think that the relative drop in profitability of value stocks is permanent. What could account for the rest of the difference?

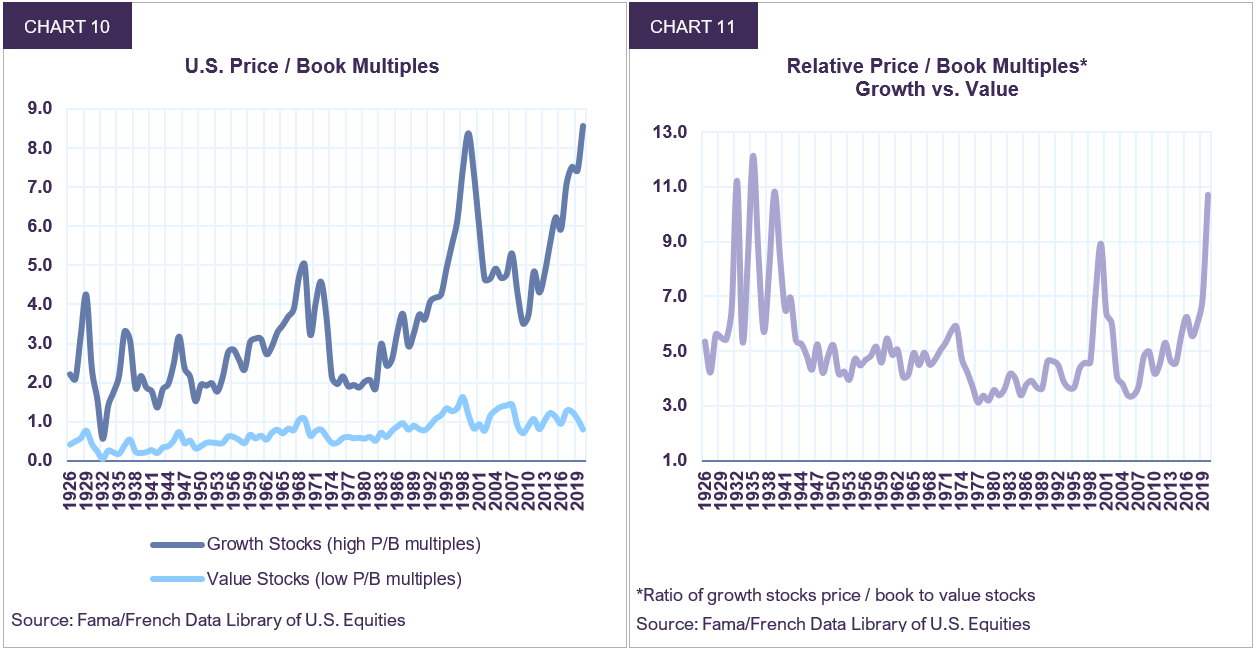

The answer is valuations. As Charts 10 and 11 illustrate, the price to book multiple of growth stocks has more than doubled since 2010. Since 2017, the relative book multiple of growth stocks to value stocks has also more than doubled. Both measures are at or near all-time highs going back almost a century.

Valuations have clearly favoured growth stocks over the last decade and one evident catalyst has been the fall in interest rates. Growth stocks derive more of their economic value from future earnings, cash flows, and investments. A fall in the discount rate (i.e., interest rate) will impact the value of outer year cash flows and therefore increase the present value of growth stocks more than that of value stocks, which depend more on near-term cash flows. But it is the drop in discount rates that has this effect. For the relative valuations and performance to continue to change, interest rates need to continue to drop, not just stay at current levels.

It is probably too early to conclude that something fundamental and permanent has changed in the normal relationship between growth and value stocks. In fact, it could be argued that growth stocks are in a bubble. Absolute and relative levels of profitability are particularly high. Relative and absolute valuation multiples are also particularly high. Interest rates are particularly low, driving some of these other records. And then there is the pandemic and consequential recession which has temporarily driven down value stock profitability.

All good excesses start with a grain of truth. Growth stocks have proven to be more resilient during the pandemic than value stocks, however the problem with bubbles is that the markets over-step by projecting current distortions well into the future.

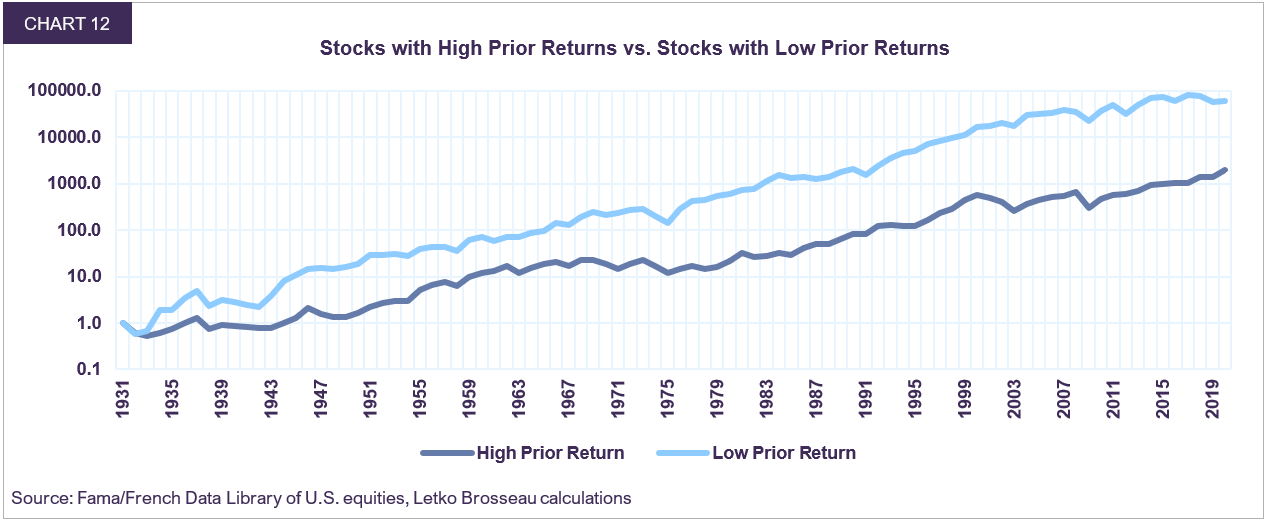

The data shows that major distortions do not last. Yesterday’s outperformers are usually not tomorrow’s outperformers, quite the contrary. Chart 12 presents the cumulative returns of portfolios invested in the top and bottom 10% performers of the prior 5 years. If a trader put $1 at the start of 1931 in the top 10% of prior performers and rebalanced the portfolio at the end of each month, it would be worth $1,929 by the end of 2019. In contrast, $1 invested in the bottom 10% of prior performers would be worth $59,200 or 30 times more. So much for investing in past performers.

Companies change, portfolios change, but not everything necessarily changes. We believe that the outperformance of growth stocks relative to value in the past decade is an anomaly, such as it was in the 30s and 90s. Profitability of value stocks will recover as the economy recovers, interest rates will rise, relative valuations will fall, and the historical relationships will be re-established.

History shows that value investing usually wins, and for good reason.

I believe my mother was on to something.

Daniel Brosseau

President, Letko Brosseau & Associates

October 22, 2020

1 – All data references to growth and value are based on the Fama/French Data Library of historical returns of U. S. equities covering the NYSE, AMEX, and NASDAQ: https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html#Research

Growth stocks are those securities whose returns ranked in the top 30th percentile of the relevant measure and Value stocks are those that ranked in the bottom 30th percentile.

2 – You can invest in the cell phone industry with a value stock. Samsung, a value stock which trades at 11 times earnings versus Apple’s 31 times, owns a greater share of the mobile phone market, builds practically everything that goes into its smartphones and has grown at only a slightly slower pace than Apple over the last few years, principally because it does not charge as much for its products.

All dollar references in the text are U.S. dollar unless otherwise indicated.

The information and opinions expressed herein are provided for informational purposes only, are subject to change and are not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. Any companies mentioned herein are for illustrative purposes only and are not considered to be a recommendation to buy or sell. It should not be assumed that an investment in these companies was or would be profitable. Unless otherwise indicated, information included herein is presented as of the dates indicated. While the information presented herein is believed to be accurate at the time it is prepared, Letko, Brosseau & Associates Inc. cannot give any assurance that it is accurate, complete and current at all times.

Where the information contained in this presentation has been obtained or derived from third-party sources, the information is from sources believed to be reliable, but the firm has not independently verified such information. No representation or warranty is provided in relation to the accuracy, correctness, completeness or reliability of such information. Any opinions or estimates contained herein constitute our judgment as of this date and are subject to change without notice.

Past performance is not a guarantee of future returns. All investments pose the risk of loss and there is no guarantee that any of the benefits expressed herein will be achieved or realized.

The information provided herein does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information.

This presentation may contain certain forward-looking statements which reflect our current expectations or forecasts of future events concerning the economy, market changes and trends. Forward-looking statements are inherently subject to, among other things, risks, uncertainties and assumptions regarding currencies, economic growth, current and expected conditions, and other factors that are believed to be appropriate in the circumstances which could cause actual events, results, performance or prospects to differ materially from those expressed in, or implied by, these forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements.

Concerned about your portfolio?

Subscribe to Letko Brosseau’s newsletter and other publications: