Canada - FR

Canada - FR U.S. - EN

U.S. - ENEquity markets moved higher during the month of May, after a slight pullback in April. Year-to-date, the S&P 500 is up 15.1% (in Canadian dollars), while the S&P/TSX rose 7.6%, the MSCI ACWI 12.6%, and the MSCI Emerging Markets 6.9%. The global economy was far more resilient than many expected in the past year, with recent developments providing further encouragement. In Canada, headline inflation slowed to a year-over-year rate of 2.7% in April from 4.4% twelve months ago. On a three-month annualized basis – a measure that reflects the underlying trend – inflation moderated to just 1.5% in the same period, less than the central bank’s 2% target. In the U.S., year-over-year headline inflation eased to 3.4% in April, down from 4.9% last year, indicating significant deceleration.

Understanding the Dynamics of Cumulative and Current Inflation

Recent Consumer Price Index (CPI) data indicates cooling inflation, with year-over-year rates suggesting a downward trend. However, consumers remain concerned over the impact of the cumulative 14.5% inflation over the last three years since April 2021. The CPI measures the average change over time in the prices paid by consumers for a basket of goods and services and is continuously updated to reflect current economic conditions. While the annual inflation rate provides a snapshot of price changes over the past year, cumulative inflation aggregates the changes over a longer period, illustrating the overall impact on purchasing power. As inflation naturally increases over time, the prices paid for goods and services years ago are unlikely to revert to previous levels.

While the impact of cumulative inflation is a key indicator to assess consumers’ purchasing power, the central bank’s objective is, instead, to control the rate of change in annual inflation. The objective of restrictive monetary policy appears to have been met as consumer prices have now returned to target levels. The impact of elevated inflation has resulted in a higher base for consumer prices, but future price increases are likely to be more modest and manageable.

Navigating Inflation: Drivers, Trends, and Market Implications

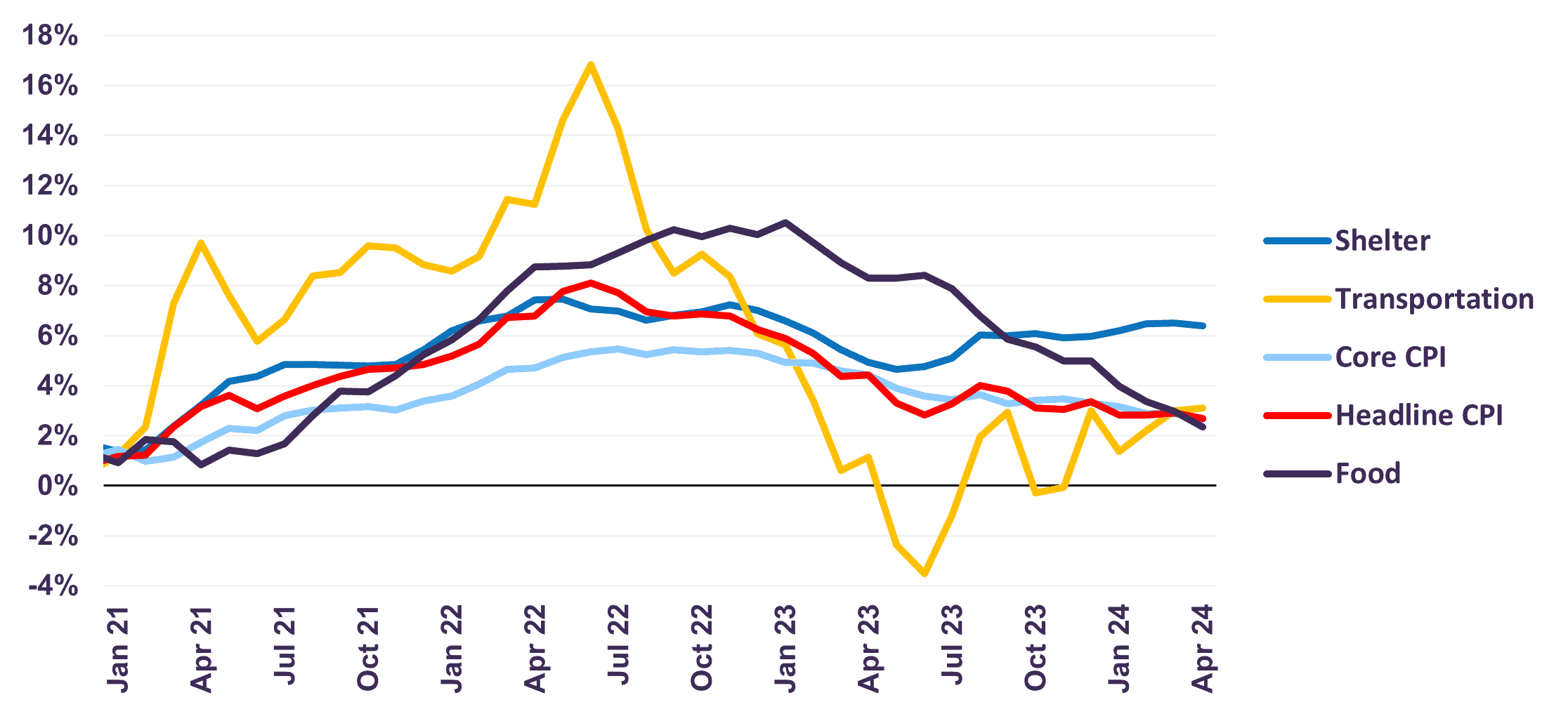

The CPI is composed of several categories that represent the share that each expense typically occupies within a household budget. The three biggest contributors to Canada’s inflation rate are shelter, food, and transportation. In Canada, the most significant component is shelter, which represents nearly 30% of total CPI. While most components of the CPI are on a downward trend, higher costs of mortgages and rents have led to sustained upward pressure on inflation. Shelter costs rose 6.4% year-on-year in April 2024 against a backdrop of higher mortgage interest rates and strong population growth (Chart 1). Looking ahead, the cyclical impact of higher interest rates on housing will dissipate as the Bank of Canada transitions to easier policy, but robust demographics suggest shelter inflation may take some time before returning to its long-term average of about 3%. Excluding shelter inflation, we believe the necessary adjustments are underway to keep inflationary pressures subdued on a sustained basis.

Meanwhile, wage growth, which typically lags or follows CPI as employees look to ensure their incomes are adjusting for rising costs or prices, has begun adjusting to the increase in inflation. In Canada, average hourly earnings are running up 5.1% in March against a year ago, significantly outpacing the CPI increase of 2.7%.

Canadian Inflation (% Y/Y)

This wage growth coupled with the deceleration in CPI results in improved consumer purchasing power. This benefits household spending and boosts consumption, a net positive for economic growth. However, recent indicators suggest that the pace of wage growth is beginning to slow, leading it to more closely align with the rate of inflation. Moreover, while softer labour dynamics will weigh on consumption going forward, spending is unlikely to collapse given the improvement in purchasing power and the elevated level of savings in Canada.

Inflation is a key economic indicator that heavily influences financial markets, shaping investment strategies, central bank policies, and investor sentiment. Among the various scenarios that can unfold within an economy, the cooling of inflation holds particular importance for financial markets, eliciting reactions across asset classes and shaping market expectations. With regards to fixed income markets, decelerating inflation leads to a decline in short-term rates as central banks bring overnight rates down and longer-term rates will also see downward pressure. However, from a long-term perspective, long-term rates remain too low when compared with fair value as determined by long-term inflation and economic growth. At present, this level is about 4-4.5%, while the 30-year federal bond yield stands at 3.5%. For equity markets, cooling inflation tends to create a more favourable environment. When the rate of inflation slows, stock multiples tend to increase as a result of lower discount rates, enhanced economic stability, and a more attractive economic backdrop.

Concluding Thoughts

While discussions surrounding inflation are both interesting and important, focusing on the long-term trends is paramount. Our analysis indicates that we are in the late stages of restrictive policy, with a transition to more accommodative measures on the horizon. Consequently, we remain vigilant in monitoring the market for potential deviations from fair value as we seek investment opportunities. Currently, our equity portfolios are well diversified across sectors and geographies, trading at a compelling 13.0 times 2024 earnings and provide an attractive 3.2% dividend yield. We are maintaining a tilt towards equities over cash and bonds within balanced portfolios, as we believe equities provide more attractive return prospects over the medium- and long-term.

Where the information contained in this presentation has been obtained or derived from third-party sources, the information is from sources believed to be reliable, but the firm has not independently verified such information. No representation or warranty is provided in relation to the accuracy, correctness, completeness or reliability of such information. Any opinions or estimates contained herein constitute our judgment as of this date and are subject to change without notice.

Past performance is not a guarantee of future returns. All investments pose the risk of loss and there is no guarantee that any of the benefits expressed herein will be achieved or realized.

The information provided herein does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information.

Certain information contained in this document constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “target,” “project,” “estimate,” “intend,” “continue” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of the strategy(ies) may differ materially from those reflected or contemplated in such forward-looking statements.

Concerned about your portfolio?

Subscribe to Letko Brosseau’s newsletter and other publications: